CoreCard Corp.

This report was originally issued in June of 2023

You can download a PDF here:

This issue I’m writing about a strange company. A strange company that operates in a very strange way. And this company, although probably unfamiliar to you, operates in an industry that is filled with hype. But the atmosphere surrounding the company is anything but hype.

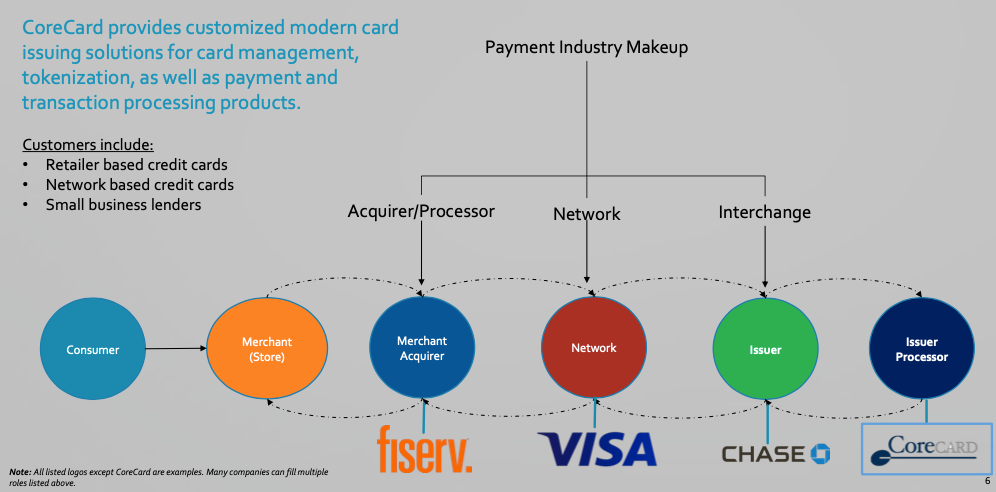

Card issuing and processing has been a pretty stable business for decades. How it typically works is that a bank (or someone like Amex or Discover) issues a debit card or a credit card to its customer. To transact with merchants, the issuers usually partner with one of the two main payment networks – Visa and Mastercard. The merchants that accept card payments are also part of the system and have to offer access to the payment network to be able to accept the card. Everyone knows Visa and Mastercard are great businesses, but behind all of this are the processors. For each transaction, a company processes the transaction for the merchant acquirer bank and the card issuer bank. Traditionally, many of these have been processed by the same companies (maybe different subsidiaries inside of the same company, but the same companies dominate both). These are typically large legacy players like Fiserv, FIS, and Global Payments.

This has all been a pretty stable environment for, as I said, decades. But things are starting to change. For one thing, more people buy stuff online, which opens the door to companies that specialize in helping online merchant acquirers process payments and access the payment networks they need to (Strip, PayPal, Square, etc.). But another part of this transition has to do with the issuing banks. You see, people have never really cared where their credit card came from – maybe it came from their bank, maybe it came from Amex or Discover, maybe it was branded by an airline. They just care what it can do for them. And, probably more than ever, people don’t trust or really like banks that much. Who they do like or trust are retail brands like Apple.

So, Apple, along with a lot of other startups and other retail brands decided it would be a good idea to issue credit and debit cards to their customers. After all, it’s a proven strategy. You might issue a card that gives customers a discount on your stuff (everyone has an app now that gives rewards), or you might partner with someone else to give the customer some kind of incentive to use your card (third-party rewards). Regardless, the goal is the same – get people to use you card so you can (1) make money off of them and (2) build your brand.

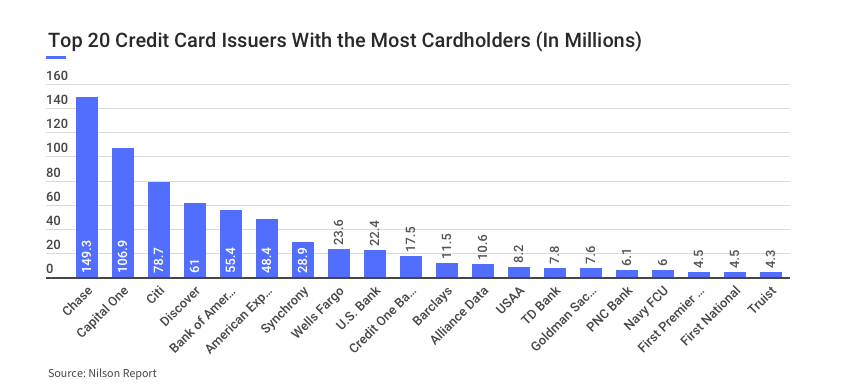

As of today, the market is still pretty concentrated. The top 10 largest card issues control 82.39% of purchase volume in the U.S. The market for credit cards is still dominated by large national banks and card companies and breaks down like this (based on the number of cardholders):

And most of these issuers go with Fiserv or FIS or one of the other subsidiaries that they own (like TSYS) to process their transactions. For instance, Fiserv handled 45% of all issuer processing last year. But there is a new subset of companies on the issuer side. Companies that aren’t necessarily traditional banks but want to create or expand a new or innovative credit card program very quickly. And that is who CoreCard Corp. CCRD 0.00%↑ focuses on.

Traditionally, most of the innovation (and competition) has occurred on the merchant acquirer side. There are still large, legacy payment processors on that side of the market, but a lot has changed over the last 20 years or so. First, there are just a lot more merchant acquirers than there are issuers. And second, the nature of their business changes a lot faster than the issuers. So, companies like Stripe, PayPal, Square, and Ayden all sprang up mostly to help merchant acquirer get better access to payment networks. Some of them may provide processing, many do not.

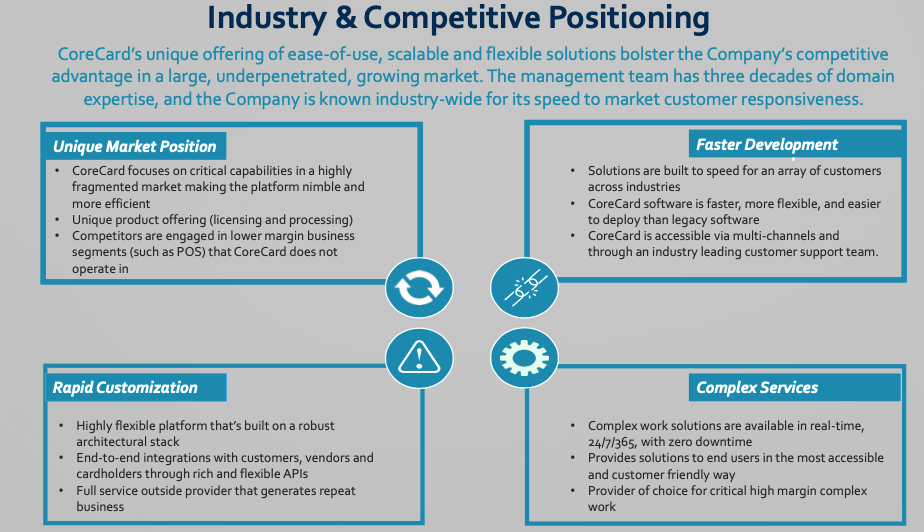

The reason I like CoreCard though is that they are operating on a side of the market with limited competition – the supply side. The merchant acquirer side of the business is obviously changing a lot faster than the issuer side. The issuer side consists mostly of sleepy banks and entrenched processors – who have been processing transactions for the same banks for the last 20 years or so. But with the growth of the fintech and non-traditional issuer market, there’s a demand for access to the traditional payment rails. CoreCard has stepped in to fill that demand, but only with higher-end credit products – their real specialty is in complex revolving credit.

Boston Consulting Group predicts that by 2030, the fintech market will capture 7% of total financial services revenue (making fintech a $1.5 trillion industry). Over the last 20 years, the vast majority of funding has gone to payments companies (25% of cumulative fintech equity funding since 2000 has gone to the payments space). And while some may disagree, I believe this is a trend that will continue. It’s hard to beat traditional banks at commercial lending – there just aren’t many ways for a fintech company to do it better. So, I think the vast majority of growth will continue to be on the consumer-facing (and particularly payments) side of the business. That’s what fintechs excel at, and that’s an area where they can take market share, or even reach people who didn’t use a traditional bank before.

This likely means more demand from new issuer entrants for payment processing. And yes, companies like Marqueta and Lithic are catering to most of these companies. They will probably continue to do so. But they’re becoming, more or less, commodity products. They may be able to get a stronghold in the market like the traditional processers did before them, but it’s very possible that new entrants will come into this API-first card issuing market (much like they did on the merchant acquirer side).

CoreCard, on the other hand, has been building and displaying (through its processing of large accounts like the Apple Card) a premium processing software that other companies can’t compete with. As the issuer market grows, I think it’s very possible that more and more customers need the premium credit processing experience that CoreCard offers. It’s possible that someone else may come into the market and create a better service/technology. But I just don’t think there’s much incentive for anyone to do that. Most of the new companies coming into the space are focusing on taking the majority of the market at lower prices – they want to capture the large number of debit card issuers, BNPL companies, and vanilla credit card issuers. The market CoreCard is operating in – while large enough to provide ample room for growth – may just be too small for many of these venture-backed competitors to go after. And who’s to say that when it comes down to it, a lot of these companies don’t just outsource processing to CoreCard (we’ve already seen it with companies like Cardless and Goldman Sachs). If some of these payment platform startups need complex processing, they may just end up outsourcing it to CoreCard.

The Business

As I said, CoreCard is a strange player stuck in the middle of this high-growth and hype-filled industry. The company offers credit card processing services, but focuses on complex and fast-moving card programs. The CEO – J. Leland Strange – claims that they have (and are repeatedly told by issuers that they have) the best credit card processing software in the world. Because of this, CoreCard charges a premium for its service, and really only goes after the subset of the issuer market that needs complex credit needs handled.

The legacy players or other start-ups can handle most vanilla credit processing needs. But CoreCard is the best at (1) getting a card program up-and-running and customized quickly, and (2) processing something like a card that would charge a different rate for someone who repaid in week 1, compared to week 2, compared to week 3, etc.

In a field of cash-burning, high-growth competitors (see Marqueta and Lithic) or lethargic legacy players (see Fiserve and FIS), CoreCard stands out for its strange business model. It employs no sales people and hardly spends anything on marketing ($336,000 total as of 2022). It has never experienced customer churn, apart from the customer being acquired or going out of business. And, most of all, it is profitable.

CoreCard has grown its revenue at a CAGR of 46% since 2017 (yeah, I know), but it hasn’t burned capital to do so. This fact is actually pretty strange when you think about the other main player – Marqueta. They are burning more cash every year, and going deeper into the red, to grow in an enterprise market. After all, both Marqueta and CoreCard aren’t actually offering cards to the public, they are going after the issuers that do – enterprise customers. Yet, Marqueta and Lithic both see fit to burn capital in the pursuit of growth here.

Source: CoreCard SEC Filings

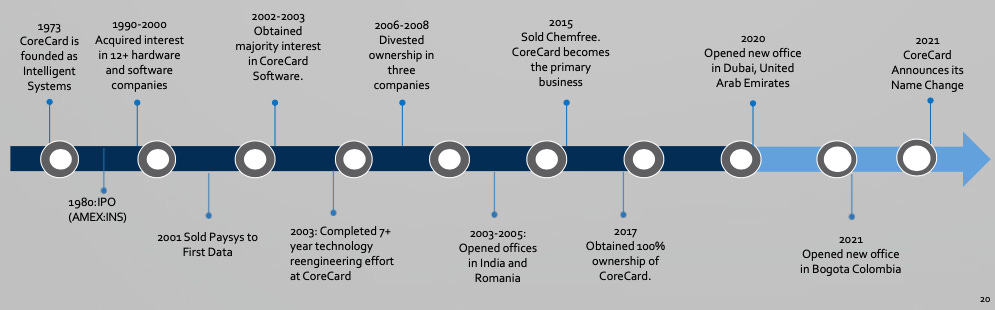

CoreCard’s roots go back a long way. The current CEO and Chairman obtained control of the original parent company – Intelligent Systems – back in 1985. The core team that started CoreCard was the leadership and engineering team at PaySys (a company that had been acquire by First Data). Somewhere along the way in 2002-2003, Intelligent Systems became involved with CoreCard (likely through an earlier investment in it), and obtained an interest in the software. It continued to focus on the company until, in 2015, CoreCard became its primary business.

Source: CoreCard September 2022 Investor Presentation

Since 2015, CoreCard has primarily been operating as the business it is today. Intelligent Systems changed its name officially to CoreCard in 2021, and has been expanding pretty quickly since it onboarded Goldman in 2018.

It may seem counterintuitive (it certainly did to me the first time I heard it), but CoreCard’s management is limiting topline growth, over time, to roughly20-25%. They have acknowledged that there is enough demand in the market for them to grow at 50%, but they don’t feel that they can. This is mainly for one reason – resource constraints. They need to have highly competent, capable employees and train them (over 1-3 years) to be able to manage a complex card program for enterprise customers. And they simply can’t hire and train enough people fast enough to grow much faster than 20-25%. They also need to continuously upgrade and improve their processing software (which they both license out to customers and use to process customer card programs themselves).

CoreCard breaks down the market they operate in as such:

Source: CoreCard September 2022 Investor Presentation

While CoreCard does operate as an issuer processer, it’s not necessarily comparable to the others in the business. CoreCard has a premium product and premium services, and it’s not competing on price. This primarily means that it’s not necessarily taking a lot of business away from the legacy issuer processors. It’s not going to take Chase or Bank of America or anyone like that away from the legacy side of the business unless something drastic happens. No, CoreCard has tailored its software and its offering to handle complex credit transactions.

In this market, debit card transactions are the simplest to process and the simplest program to manage. And it makes intuitive sense if you think about it. You’re just matching up the customer’s bank account at the issuer to the merchant’s bank account. But on the credit side, you’ve got money being lent by the issuer, you’ve got (potentially) different payment terms depending on what the customer does or who the customer is, you’ve got different limits on different accounts, etc.

Source: CoreCard September 2022 Investor Presentation

CoreCard can handle all of that. In fact, it positions itself to handle new and innovative card programs quickly. It’s no secret that CoreCard’s biggest customer at the moment is Goldman Sachs. They brought Goldman on as a customer in 2018, and in FY 2022 Goldman represented 75% of CoreCard’s total revenue. What is this Goldman account? Mostly, it’s processing for the Apple Card – the most successful new credit card in history. It’s also, more recently, licensing and processing for the GM fleet card. But let’s focus on the Apple Card part of it.

What does it say about this company that arguably the most important card program launched in the 21st century chooses CoreCard to be their processor? Yes, they’re going through Goldman (which is a great client to impress), but don’t think that Apple doesn’t have a say in things. Apple and Goldman are using CoreCard’s technology because they wanted to create a new custom card program quickly. And that’s what CoreCard does.

Even though you’ve probably never heard of CoreCard before now, it has a list of innovative and A-list players as customers. Yes, they’ve definitely got some regional and community bank card issuers too (and that’s an important part of the market), but a lot of their future growth is probably going to come from the fintech/non-traditional side of the market. Some of CorCard’s main program manager customers (that use CoreCard for processing) are the cloud card companies – Cardless, Deserve, and Vervent. CoreCard also handles Amex’s Kabbage credit program (and handles Kabbage’s legacy business that they started processing before the Amex acquisition) as well as new programs that Amex is establishing with Simon Properties and Cardless.

CoreCard has a connection with the Visa, Mastercard, and Amex payment networks, so they can handle cards for pretty much any issuer in America. They just recently connected with Amex in Q4 2022, so that should drive some additional revenue from issuers who couldn’t use CoreCard before the connection.

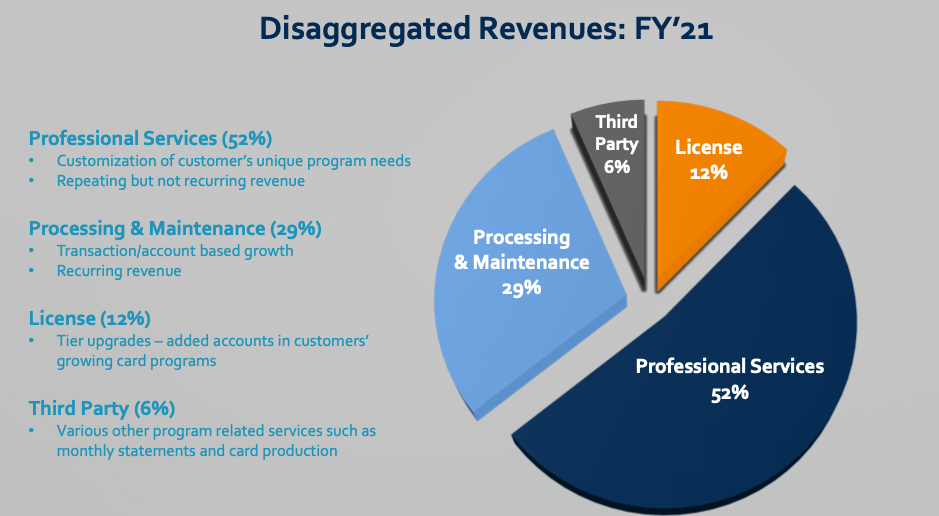

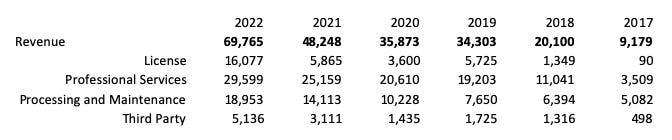

CoreCard’s revenue breakdown in a normal year looks like this:

Source: CoreCard September 2022 Investor Presentation

The revenue was distorted some in 2022 from one-time licensing revenue as a result of the GM conversion, but in normal years, professional services make up roughly half of total revenue. As it grows, CoreCard’s been trying to grow its processing and maintenance revenue to become a larger part of its business, considering that is really the only portion of its revenue that’s truly recurring.

Source: CoreCard 10-K Filings

CoreCard charges processing fees based on the number of cardholder accounts in a single program. So, it’s not necessarily subject to the fluctuations of payment volume year-to-year, but it doesn’t get the upside that other processing networks might if volume increases rapidly. CoreCard only grows its processing revenue if accounts at its customers grow – true brand growth at the customer.

Overall, CoreCard’s revenue is really driven by two types of customers. It brings on a number of smaller card programs from smaller issuers that desire the customization, flexibility, and complex credit processing that CoreCard offers. Many of these are fintech companies and/or non-traditional issuers and many are smaller regional and community banks. These may not generate as much revenue up front as a larger licensing deal or larger customer, but CoreCard can generate processing and maintenance revenue from them as they grow. Obviously, some of these card programs (perhaps many) will fail or not grow at all. But some may turn out to be much bigger than they were when they started.

The other side of the coin is the large accounts that CoreCard services. Obviously the largest is Goldman, but there are others like Amex (in certain business segments) and PAX. Occasionally, CoreCard will close a deal with a larger customer and increase their processing, professional services, and sometimes licensing revenue much faster than they did in the past. But these deals take time and may not work out. This means that revenue can be lumpier than other segments. For instance, CoreCard courted a relatively large customer throughout 2022, expecting to close a deal in the fourth quarter. But the customer eventually backed away. That happens, and the sales cycle for these larger deals is long. In fact, it’s hard to even call it a sales cycle because CoreCard doesn’t employ any sales people. They just operate at the top of the industry and eventually word gets around to a large player, or a large player acquires a company they’re service and they like what they see (as happened with Goldman and Amex).

Operations

CoreCard, as a software/consulting business at the moment, is pretty capital light. It typically generates an ROE of over 20% (~26% in 2022), and this climbs even higher if you back out cash (which makes up roughly a third of total assets, but has made up two-thirds in some years). The company doesn’t have very much in the way of assets on its balance sheet, and it doesn’t appear to capitalize software development costs. So, there are no real capital requirements associated with growth if you think about it. Obviously, there is some required capex in PP&E, but this seems to be mainly in premises related to employee expansion (as it has increased recently). A very small part of CoreCard’s PP&E is dedicated to capitalized software costs or intangible assets.

CoreCard’s gross margins have remained above 50% for most of its recent existence (i.e., when CoreCard was the main business), but they bounce around a decent amount. Operating margins and net margins are typically more volatile, with operating margins sitting at close to or above 30% in most years and net margins at close to or above 20% in most years.

CoreCard’s management team, in contrast to the vast majority of management teams you will see, doesn’t really focus on margin targets. Inevitably, on almost every earnings call, Leland Strange gets asked what he think margins will be in a certain year or quarter, and every time he responds by saying that he’s not worried about margins – he’s worried about growing to be a large and profitable business. It’s an interesting take from an extremely profitable company in a sea of money-losing startups. But I honestly think it’s the right take. Focus on what matters.

CoreCard’s expense base and product mix cause margins to fluctuate. Licensing revenue, for instance, basically has no cost associated with it, so it goes straight to the bottom line. But it’s lumpy, staying small most quarters and ramping up every once in a while. Processing revenue and professional services revenue both have lower margins associated with them as they have labor (professional services) and technological/structural (processing) costs associated with them. But they are much more predictable (processing revenue especially), and you don’t have to replace your entire revenue stream with new services or customers every year just to maintain.

CoreCard currently has about 1,200 employees worldwide, with the vast majority of these being in places like India, Colombia, Romania, and the UAE. As I’ve already said, CoreCard doesn’t really spend any money on marketing or sales, and its G&A is also surprisingly low, at 7.3% of total revenue in 2022. Roughly 1,100 of these employees are R&D and testing employees. CoreCard spends a decent amount of time and resources on improving its software (probably more than anything else). Since it is known for having the best software for complex credit processing, it wants to continue to solidify its reputation and position. A decent number of CoreCard employees also appear to be involved in providing professional services to clients, so the cost of their labor is (at least partially) included in costs of revenue.

CoreCard has been expanding its workforce overseas for years. In 2021, they opened an office in Bogota, Colombia to support existing customers and help with future growth (mainly in the U.S. I assume). In 2020, they opened offices in Dubai to help with growth in the Asian Pacific and the Middle East. In 2017, they opened their second office near Mumbai, in India, to attract the kind of talent they need for software development and support for growth.

All of this has resulted in net income in 2022 that was just over $13 million. Even with the contribution from licensing revenue, the net margin was just under 20% – around average, but lower than some other years as well. As I said, above, CoreCard has recently incurred slightly higher capex, and its increase in receivables (as the business has grown faster) has also eaten away at FCF. Right now, CoreCard’s cash flow conversion isn’t that great. It’s been high in the past, and I assume a lot of the capex and receivables growth is somewhat (if not all) temporary.

Going Forward

CoreCard’s focus for the future is on building out the processing side of its business. While not abandoning the other parts of its business, CoreCard wants to focus primarily on becoming a credit card processor. To do this, it has been investing in its processing infrastructure, driving overall margins down, but expecting this to result in economies of scale as it grows.

So far in Q1 2023, CoreCard’s overall revenue is down close to 40% (compared to Q1 2022) primarily as a result of the large licensing income in Q1 2022 (the entire GM conversion was booked in that quarter) and the absolute lack of licensing revenue in Q1 2023. Services revenue, though, was actually up by 25% YOY in Q1 2023. As a component of that, professional services revenue grew by 27% and processing and maintenance grew by 33.7%. Third-party services shrank slightly, but it’s such a small component of overall revenue, that it hardly made a difference.

Because of the lack of licensing revenue in conjunction with the increased hiring in India and increased spend on digital infrastructure, operating margins dropped to under 12% in Q1. CoreCard management noted in the Q1 2023 earnings call that they expect to slow down hiring for a while (after the large uptick over the last three years), but they don’t expect to pause the increased software spend in the near future. In addition, they don’t expect any significant licensing revenue for the rest of the year (though there’s a possibility in Q2)

Be warned, 2023 could be a slower year for CoreCard. Even though they had services growth of 25% in Q1, they’re only guiding for 10% services growth for the year and no growth in products revenue for the year. They’ve indicated that it’s a relatively slow environment now for card launches and conversions, especially in the banking industry. With the backdrop in banking the last few months, management has explained that no regional banks are going to come launch a new card with them. A few community banks might, but no larger banks are going to convert their card program or launch a new card in this environment.

That being said, CoreCard has a history of under-promising and over-delivering. Strange has even said that this guidance is very conservative and doesn’t take into account any new accounts. It especially doesn’t take into account the potential for closing new large accounts – which CoreCard has indicated it may do (2 large accounts possibly) near the back half of 2023. The company has been gearing up with hiring and investing in its infrastructure so that it can service more larger accounts – it’s not just going to steadily drift along. They didn’t have the capability throughout 2022 to add any more than one more new large account, but by 2024, they will be able to add three or four.

This is mainly because of their expansion in personnel. CoreCard added 300 new employees in 2022 (most, if not all, of them overseas), and have been expanding their workforce at a much faster rate than usual over the last four years (from 430 employees to 1,200). Management has noted that they will slow down hiring significantly in 2023, as they’ve reached a point that can support their transition.

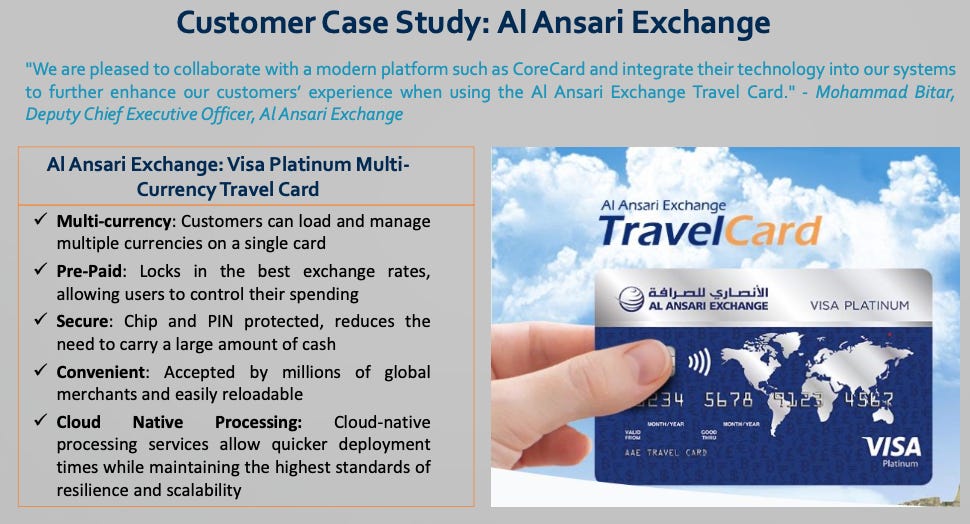

Though the vast majority of revenue does come from U.S. companies, I think there is also some room for expansion overseas. CoreCard has a lot of talent and now some experience in foreign countries. Part of the reason it’s opened offices in the Middle East was to reach areas like that as well as the Asian Pacific area. And it’s landed a few accounts. For instance, the Al Ansari account is right up its alley. Handling complex credit transactions where the card itself determines the best exchange rate is definitely something that I could see CoreCard expanding into.

Source: CoreCard September 2022 Investor Presentation

CoreCard expects its margins to be lower for the time being – management has guided gross margins to somewhere around 30-40%. In Q1 2023, CoreCard’s gross margin was 33.5%, its operating margin was 11.3%, and its net margin was 8.5%. This is a lot lower than the past few years, and I’ve discussed some reasons why this particular quarter was lower and why margins will be a little lower than normal for the foreseeable future.

Management

CoreCard’s management has an impressive track record, and they are heavily aligned with shareholders. As of 2023, directors and officers as a whole own 16.4% of the company, with J. Leland Strange (the CEO) owning 15.3% of shares outstanding. The next largest shareholder is Clifford N. Burnstein (appears to be a private investor) who owns 9.8%, and Weitz Investment Management (run by the investor Wally Weitz) who owns 6.9%.

Management is definitely unorthodox – you just need to listen to or read a few earnings calls to understand that. Strange has been in the software business since 1980 (founding Quadram Corporation), and has been the CEO and Chairman of Intelligent Systems (which later acquired and became CoreCard) since 1985. So, Strange has been operating in this business for a while, and seems to have a good reputation among issuers looking for a processor that can handle complex card programs.

As good a CEO as he is, though, Mr. Strange is now 81 years old. He owns the largest position in the company, and he appears to be a major draw for customers (considering the small amount of employees they have, including no sales personnel). There could be some serious key-man risk here, but if I had to guess, Strange has recruited Matthew White (the CFO) to one day succeed him. It’s obvious from the earnings calls that White plays a role in the operations of the company (even though he is technically the CFO). He answers nearly as many questions as Strange on the calls, and he appears to be very knowledgeable about the business.

I obviously can’t say for sure how things will play out, but if I had to guess, I’d say that Strange will probably stay CEO for as long as he can – he doesn’t seem like someone who is interested in retirement – and the CFO Matthew White will one day succeed him and continue to operate the business in the same manner.

Risks

Customer Concentration

The biggest risk is the most obvious risk. Goldman is over 70% of CoreCard’s revenue, and will remain that high for the foreseeable future. That means that, as it stands, CoreCard’s near-term future is almost completely reliant on Goldman. Yes, it can grow its processing revenue from other customers (and it’s been doing that), but customer concentration this big always leaves it open to risk.

Strange has said that when he’s asked about customer concentration, he’s happy to have a customer as large as Goldman. And there is an upside to that. CoreCard is now known around the industry as the company that processes the Apple Card. That’s probably resulted in, and will result in, more future business opportunities. And it shows everyone that CoreCard can handle a large account.

But that doesn’t change the fact that there is pretty big risk around this account. Up front, I will say that I don’t think the Apple Card is going away. I don’t know a ton about the GM program, but the Apple Card is here to stay. The question really revolves around (1) Apple’s decision over who will handle the technical aspect of the program, and (2) CoreCard’s relationship with Goldman as the middle man.

The first potential risk is that Apple may decide to go with someone else as its processing partner. Or, as a 2022 Bloomberg article alluded to, it may bring the processing and other technical aspects of the card in-house. It’s been over a year since that piece was published, and nothing has yet to come of it. Strange addressed the issue in CoreCard’s Q1 2022 earnings call, and he basically said he has no reason to believe that Apple won’t keep using Goldman to run their Apple Card program for years to come. If you read or listen to the transcript, you can tell that Strange is a very sharp operator. He pointed out that it would be more expensive and time-consuming than most people know for Apple to rewrite the software that processes their card and runs their program. He also noted that CoreCard and Goldman have been extremely flexible and nimble with this card program, and that, by all measures it was the best credit card debut in history. But, ever the realist, Strange does point out that large corporations act illogically, and that you would be a fool not to expect them to act illogically.

The other side of this debate focuses around a potential acquisition by Apple or Goldman. After the initial fear from the article, some rumors started to surface that Apple was planning on purchasing CoreCard – that was (in some people’s minds) how they were going to bring the processing in-house. But nothing has seemed to come of it, and to be honest (as an investor) I don’t really want an acquisition. Don’t get me wrong, a buy-out at a high price would be great, but I’m looking for multibaggers – companies that can compound for long periods of time. I think CoreCard is one of them, and a buyout would stop that compounding short. But, given the option between Apple leaving or buying out CoreCard, I may be inclined to wish for a buyout. As I said, though, that has been over a year ago, and there has been no more news that leads me to believe that Apple is leaving Goldman or CoreCard.

It is true, however, that Apple has started new payment programs (like the BNPL and Savings Account) without using CoreCard as a provider. This could hint at a potential move, but as far as I know, it’s not in the cards for right now.

The other main risk associated with this is Goldman. Everyone knows that Goldman’s entrance into the consumer banking business has been less than stellar. They have been consistently losing money in the consumer business, and they have, in fact, announced – on June 1, 2023 – that they are winding down their consumer business (Marcus, I assume) in the near future. But, from all appearances, they are sticking with the Apple program. Even though they have apparently lost moneyon the Apple Card, it does seem to be the bright spot of their expansion into the consumer banking market. At a 2023 conference, Goldman had this to say about the Apple relationship:

“We feel good about the Apple partnership. It's a very strong relationship. Apple is an important client of the firm, they're important partner to the firm. That is an extraordinarily powerful ecosystem. I mean, it's just continues to amaze me when you think about what that ecosystem can deliver. And so we're privileged to be a partner with them and to be able to -- to be valuable to them, we think in the context of providing services, banking services to their customers. So we feel good about it. It's going well. And we're continuing to invest in the partnership and the relationship. And we're trying to do our part to be an ever better partner to run the business, the credit card business as well as we can. We think we can make it more efficient and more profitable over time and we're working hard at that.”

As far as I can tell, Goldman realizes the value and future potential of the Apple Card and other programs (like GM) it may manage. If there’s any takeaway from its foray into the consumer banking business, it might be that it’s better off as an issuer-bank or program manager for card programs from other brands.

Competition

Another risk that hasn’t really been a factor for CoreCard in the past but may become an issue in the future is competition. I’m not talking about competition in the overall issuer processing market – that has always been there. But competition from some kind-of start-up or merger between potential competitors.

CoreCard’s management is correct in noting that they themselves – for a lot of the accounts they go after, but not all – don’t face much real competition. If a potential customer is worried about price or isn’t right for CoreCard, they are fine with losing them to a commodity-like processor. But this attitude – while it has served them well so far – may not suffice if more competition comes into the industry.

Now, I’m not one to criticize how management operates. There’s no way I could tell them what to do or how to do it. My job is to find the best management team operating the best business that I can buy at a reasonable or cheap price. But I will note the risks inherent in how a management team operates – especially if there may be structural changes coming to a market.

There are some pretty active and innovative new entrants in the market – namely Marqueta (who CoreCard has acknowledged as a competitor, though not really direct competitor) and Lithic. Marqueta is now public and you can check out their business and how fast they’ve grown (they now process $166.3 billion in payment volumes). Marqueta is more focused on being an API-first platform for issuers, which basically means that they’ve created an entire platform where they can (1) roll-out and manage a card program (even down to the issuer bank) for fintechs or (2) the fintech company itself can pay to access the Marqueta platform and run its own custom card on it. Marqueta isn’t necessarily focused on being the best processor, but processing is included in its services. It is competing with CoreCard, to some extent, but in my mind it’s probably competing more with a company like Cardless – offering outsourced card issuing and program management services to non-traditional issuers. Marqueta is the only other independent publicly traded competitor to CoreCard.

And if you’re worried about CoreCard’s customer concentration with Goldman Sachs, Marqueta is basically employing the same model. Roughly 70% of its volume is derived from Block (which has its own set of problems). Marqueta, like many other tech companies, has also recently announced that it’s laying off roughly 15% of its workforce. Amazingly, Marqueta spent over $147 million in the first quarter of 2023 alone on compensation and benefits. That’s more than all of CoreCard’s revenue for 2022. CoreCard, by comparison spent just over $5 million in G&A and just over $11 million in R&D in FY 2022. But get this, CoreCard has 1,200 employees total and Marqueta has 974. It actually has less employees than CoreCard and spent an exponentially larger amount on them in just the first quarter of 2023. I honestly don’t know how to comprehend this. CoreCard is obviously smaller on a revenue basis (so Marqueta generates a lot of revenue per employee), but you can see the difference in costs of locating in Georgia (versus California) and primarily hiring internationally. So, take your pick, an unprofitable commodity-like processing company with a large customer concentration or a profitable premium processing company with a large customer concentration. I think I’d rather have the Apple Card.

Lithic also operates much like Marqueta. Both of these companies have tried to take the business model that companies like Stripe and Ayden revolutionized on the merchant acquirer side (though I don’t think Stripe really processes payments), and apply it to the issuer side of the market. Lithic, as Packy McCormick discusses in this detailed piece, has actually been growing even faster than Marqueta. The company is trying to essentially build completely outsourced issuing and financing infrastructure mainly for the non-traditional banking industry. I think a company like Lithic could be a potential threat – if only for the fact that I don’t understand this technology enough to know if they could create a platform that will effectively replace CoreCard. CoreCard has made arguments as to why it would be difficult to do this, and payments is notoriously difficult to break into, even if it looks easy from the outside.

The other main players in this market are Galileo and Stripe Issuing. Galileo is owned by Sofi and offers an API platform for a lot of the larger, earlier fintech companies. Stripe Issuing is more focused on commercial card programs, which could eat into CoreCard’s business. But I think they’re more focused on the small business card issuing market, whereas CoreCard is mainly focused on consumer credit (though not solely focused – see the Kabbage business).

Source: Not Boring – Lithic’s New Customer

Judging from the Not Boring breakdown, I’d say Lithic may actually be the best positioned to challenge CoreCard, as it’s focused on the more modular, customized end of the market. Overall, I don’t exactly know how things will play out. For now, CoreCard seems to be differentiated enough that it’s not facing serious pressures from these companies. And, I don’t want to get ahead of myself, but there’s a possibility that some of these companies may not stick around for very long. CoreCard, however, is in it for the long-haul and will continue onboarding the right customers for its product and services.

Valuation

When it comes down to it, you’ve got to ask yourself what could CoreCard really do. They’re trading at a roughly $215 million market cap as I write this. That’s a 15x multiple on 2022’s net income, and likely higher on 2023’s (lower margins, though an increase in revenue could drive earnings higher). CoreCard’s revenue is lumpy, but management has indicated that 20-25% revenue growth annually over the long term is what investors should expect. Can they generate higher growth? It’s possible, but if Strange says don’t count on it, I wouldn’t count on it.

What could future growth look like at CoreCard? Well, it’s hard to say, but we can for sure model a 20% growth rate scenario and make some assumptions to see what happens. If, after 8 years, CoreCard’s revenue grows at a 20% annual rate, its net margins are at 15%, and it is still trading at a 15x multiple, you would have a company worth roughly $675 million. That’s an increase of 3x over 8 years, or a CAGR of close to 15%. Is that doable? I think definitely think so, and this is assuming margin compression over time.

The demand is definitely there. In fact, if CoreCard could figure out a way to grow faster without sacrificing their franchise or profitability, I think it would be relatively easy for them to grow at a 25% or 30% rate over time. They estimate that their TAM is $33 billion, but I don’t really know if this is limited to just their specialty market or the entire issuer processing market. As it stands, there doesn’t really seem to be anyone who can challenge CoreCard at its own game. There have been no major processing entrants on the issuer side for roughly 20 years. They list Marqueta as their only real competitor, and, while they have grown fast, are more of a commodity product that competes on price, not with CoreCard.

In addition to the potential for improved growth, there’s a good possibility that CoreCard could put up better margins in the future too. After all, it has expanded its workforce enough to handle larger customer accounts and a greater number of overall customers. And it is engaging in a heightened investment in software infrastructure that will presumably allow it to scale its processing business in the future. I don’t think it’s unreasonable that CoreCard’s net margin could be 20% or higher in the future even without a lot of licensing revenue.

One of the best things about Corecard’s growth, though, is that it won’t require much if any capital expenditure to fund it. Like a lot of software companies, CoreCard doesn’t have to really invest in equipment or other capital to grow. It has expanded its operations lately (mostly employee and premises adds), so capex has been a little higher, but most of the elevated spend is behind them. Now that they have the resources to service more accounts (especially more large customers), they don’t need to invest any more to grow. Think about it, the company doesn’t spend any money on marketing, it really doesn’t need to invest in new property or equipment to grow, and it’s already profitable even with the relatively large number of new employees it has had to onboard over the last four years. CoreCard really just waits around for customers to come join it program. And with the current infrastructure being built out, it won’t have to make any more significant investments to service those customers.

Conclusion

Overall, CoreCard is an impressive business that operates in a high-growth niche. It’s got a great management team that has a history of profitable growth, and it’s a capital-light business that offers a differentiated, premium product. I think 20-25% growth (even if it is lumpy) with little to no capital requirements going forward is every investors dream.

But there are obvious risks associated with this. While the large customer concentration is arguably the best piece of marketing the company has ever had, it’s a huge risk at roughly 70% of revenue. If CoreCard loses this account, the business would be devastated. On the other hand, if CoreCard can continue to grow out and diversify it’s processing business, I don’t see any reason why it wouldn’t receive a higher valuation from the market in the future (though I’m not counting on it).

What makes a multibagger is really consistent, profitable growth. No matter what the media or Silicon Valley says, there are very few long-term multibaggers who weren’t consistently profitable for a long time. You can’t burn money forever and generate great returns. I think CoreCard embodies this ethos, even if on the surface it’s not outwardly focused on growth or “innovation” as some other players in the market. It operates in a market that relatively restrained in terms of competition and it (for now) offers a product/service that no one can compete with.

This Publication is for informational purposes only, and nothing we say should be taken an investing advice. Past performance is not predictive of future returns. If you are considering a purchase of securities, please consult a licensed financial advisor. This is not a solicitation or an offer to buy any of the securities mentioned. This is not advice to buy, sell, or hold any of the securities mentioned. The author of this Publication may have positions in the securities mentioned or may initiate a position in the securities mentioned in the near future.